CyberPolicy is monitoring news of the coronavirus (COVID-19) outbreak and has activated a business continuity plan in response to the situation. We have implemented precautionary and preparedness measures to reduce exposure to the coronavirus and are prepared to maintain normal business operations.

X

Contractor Insurance Policy: What to Look For In Your Coverage

As a contractor running a small business, you know that finding a cost-effective insurance policy is a priority. However, navigating the insurance process can be more challenging than you may have anticipated.

As a result, many contractors may buy from the first insurance provider they meet with to save them the time of shopping around. If you’re not in the know about what you need from a contractor insurance policy, this may leave you vulnerable to costly risks that could deplete your personal or business assets.

So, how can contractors make sure they’re getting an insurance policy that covers all of their needs? Knowing the types of insurance you’ll need, common exclusions, and how to navigate the insurance process is a good starting point.

Types of Insurance Policies Contractors Should Have

Whether you’re landscaping gardens or putting roofs on houses, your daily operations often take place on someone else’s property. This makes your company liable for third-party injury and property damage.

You also have employees, subcontractors, or both helping you out with different business processes, and you have equipment you’re responsible for.

Here are three of the most common types of contractor insurance policies that cover the risks that come from these factors.

Liability Insurance Policies

A dependable liability insurance policy will cover any third-party damages that could cause you excessive financial loss. These scenarios include third-party property damage, injury, and failure to complete a job.

Here are two types of liability insurance that all contractors should consider investing in.

General liability insurance in a contractor insurance policy protects you from financial loss or damages due to medical expenses, property damage, libel, slander, bodily injury, lawsuit defense, and settlement bonds or judgments.

Contract surety bonds involve a third party that ensures work gets done. If you, the contractor, fail to finish a job, the surety company must find a new contractor to do the job. Contractors appreciate surety bonds because they enable them to give an added layer of security to their clients.

Workers’ compensation insurance covers the cost of lost wages and medical bills for employees who get injured at work. An important distinction for contractors when buying a workers’ compensation policy is that you need to provide workers’ compensation only to employees, not subcontractors, even if you use both in your business.

If you only subcontract work, a workers’ compensation policy isn’t necessary for you.

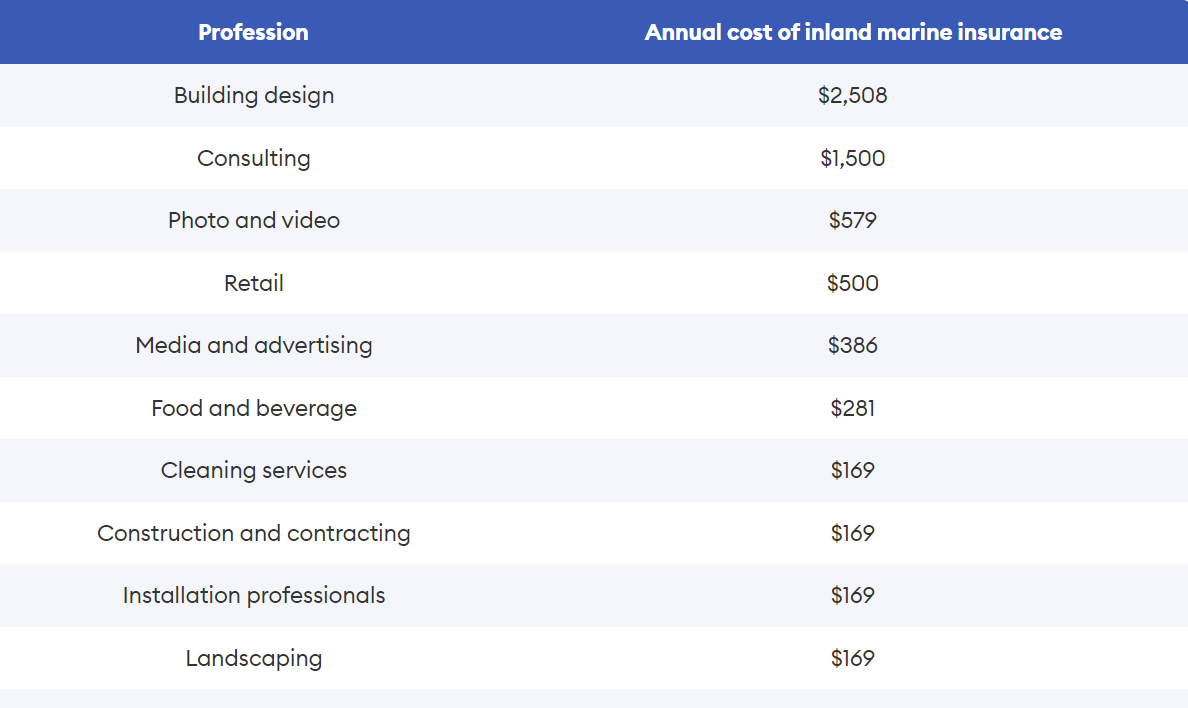

Inland Marine

Inland Marine insurance covers equipment, products, materials, and tools while they’re stored at off-site locations or in transit over land. An inland marine insurance policy is vital for contractors with equipment or products they store off-site or transport regularly. Inland marine can protect your assets from vandalism, theft, or even fire!

Annual Cost of Inland Marine per Industry, Forbes Advisor

Significant Exclusions and Limitations to Look Out For

A key piece of finding the right insurance policy is knowing what’s not included. Here are some common exclusions to ask about.

Tools are rarely covered under general liability insurance policies. General liability covers third-party damages, not damages to your property. To ensure tools are covered, ask about general liability exclusions and consider a policy like inland marine, which does cover tools. You could also consider a business owner’s policy, a bundle of insurance policies customized to your business needs.

Cyber liability coverage has become commonplace for all small business owners to hold. It can protect you from damages due to data breaches. However, cyber liability is typically excluded from other liability policies. If you use technology in your daily operations, cyber liability is worth looking into as a standalone policy.

Pollution liability, also known as environmental insurance, protects you from financial damages due to unintentional environmental damages. Coverage for pollution-related accidents is typically excluded from other liability policies. If you think accidental pollution may be a concern for your business, you should inquire about standalone pollution liability policies.

These are just a few common examples of exclusions. To ensure that you’re adequately covered in the case of any potential risk, be clear with your insurance provider about all of your risks and ask about policy exclusions.

Understand How to Get the Most Out of Your Coverage

Part of knowing what to look for in your contractor insurance policy is understanding what you can expect from a policy with your budget and exposure. Before you start looking at insurance policy options, sit down and make a list of your day-to-day exposures.

Ask yourself questions like:

What risk is inherent in my daily operations?

How much money do I have in assets?

What assets will I need protection for?

How many people do I employ?

Does my team routinely work in risky environments?

By addressing your exposure to risk, you gain a thorough understanding of what will determine your overall insurance cost, including premium and deductible costs.

Once you have a better understanding of the risk you bring to the table, it’s time to start getting insurance quotes. It is possible to find a thorough coverage option that’s also budget-friendly. The key is getting quotes from several people. By talking to several different insurance carriers, you can find the best policy option for your business.

Weigh factors like premium costs, deductible costs, and coverage limits when deciding which plan to choose. Your insurance carrier may also be able to give you a payment plan to make your premium payments more manageable!

If you feel unsure about the insurance process, consult an insurance expert like our team at CoverHound when buying your contractor insurance policy.

Now You Can Find the Best Contractor Insurance Policy

There are several types of insurance policies a contractor should invest in, from liability insurance to workers’ compensation and inland marine. By choosing policy options that cover risks in any situation you may be in, you’re protecting your business – now and in the future.

When you’re shopping around, remember to ask about exclusions, take stock of your exposure to risk, and get several quotes for the best policy option for your budget and business needs.

When you use an all-in-one online insurance platform like CoverHound, you can shop for different policy options from qualified providers in one place. CoverHound provides users with fast, accurate, and actionable quotes.

Learn more about how CoverHound can help you find the right contractor insurance policy and coverage!